[CUB] – California United Bank announced the promotions Monday of Sam Kunianski, Stephen “Steve” Pihl and William “Bill” Sloan to Executive Vice President. Mr. Kunianski manages Commercial and Private Banking and Mr. Sloan is the Santa Clarita Valley Regional Manager and leads Real Estate lending for the company. Mr. Pihl has joined California United Bank from Premier Commercial Bank (acquired by California United Bank effective July 31, 2012) and has been named the Executive Vice President of the Orange County Market.

David I. Rainer, President and Chief Executive Officer of California United Bank and CU Bancorp, stated, “Both Sam and Bill have made significant contributions to the growth and expansion of our Bank. Sam joined us in 2006 and quickly took the reins of commercial lending, consistently building our business across all of our offices and establishing a strong foundation from which the Bank continues to grow. Bill has been with California United Bank since the Bank’s inception in 2005, and his leadership in the Santa Clarita market, as well as his management of real estate lending, has been integral to our success. Steve brings to California United Bank a well-rounded record of accomplishments in independent banking with an emphasis on lending and credit administration, and his community involvement in Orange County is extensive. On behalf of our Board of Directors and all of our employees, I congratulate these seasoned leaders and enthusiastically welcome them to our executive team.”

Sam Kunianski

Prior to joining California United Bank in 2006, Sam Kunianski was head of commercial banking for US Bank in the Los Angeles Market in California and at Santa Monica Bank, which was acquired by US Bank in 1999. Before joining Santa Monica Bank, Mr. Kunianski was head of commercial banking for Pacific Century Bank.

Mr. Kunianski holds a Bachelor of Science degree from the University of Colorado, Boulder. He serves on the Board of Directors of Inner City Arts in Los Angeles and is a former director of The Boys and Girls Club of Santa Monica as well as the Santa Monica YMCA.

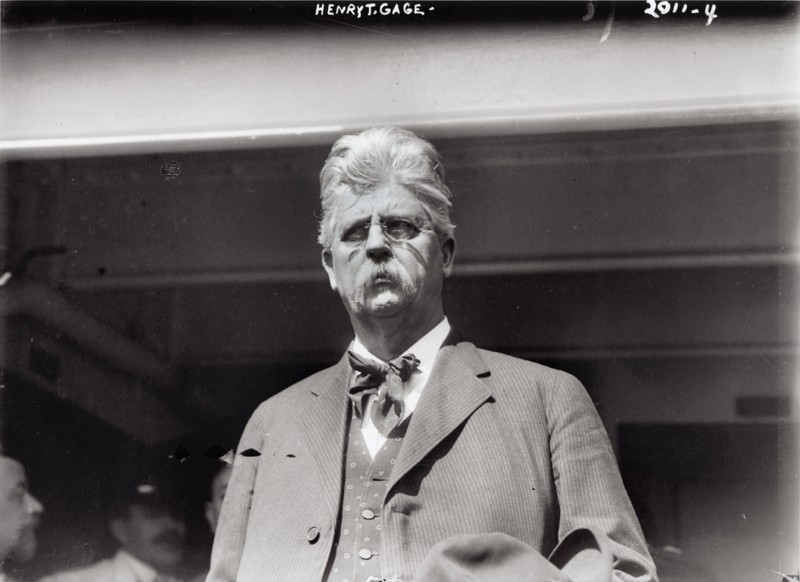

Stephen Pihl

Steve Pihl is a seasoned banker with over 25 years of commercial banking and SBA lending experience in Orange County. After a number of years with two successful independent banks, he spent over 10 years with Orange National Bank serving as first vice president and manager of the Stadium Office. Prior to joining Premier Commercial Bank as its founding Chief Credit Officer in 2001, Steve held an interim assignment with California Bank and Trust (acquirer of El Dorado Bank) in their Corporate Lending Group.

Mr. Pihl is a graduate of California State University, Fullerton with a bachelor’s degree in finance and a graduate of the California Banking School and the Pacific Coast Banking School at the University of Washington. He currently serves on the California State University, Fullerton Executive Council and the St. Joseph Hospital Foundation Board. He previously held board positions with the Anaheim Chamber of Commerce, the Consumer Credit Counseling Service of Orange County, the Anaheim Family YMCA, and Rotary International in Anaheim.

William Sloan

William Sloan joined California United Bank at inception in 2005. Earlier, he was a senior vice president with US Bank, leading the Los Angeles real estate banking operations in Southern California. Mr. Sloan was a senior vice president and head of commercial real estate for Santa Monica Bank until 1999 when US Bancorp acquired the bank and its holding company Western Bancorp. Mr. Sloan joined Santa Monica Bank via an acquisition of the Bank of Los Angeles where he was a senior lender and involved with other bank acquisitions before the company was sold to Western Bancorp in 1998.

Mr. Sloan obtained a Bachelor of Science degree in economics from California Polytechnic State University at San Luis Obispo and holds a degree from the Graduate School of Community Bank Management at the University of Texas. Mr. Sloan serves on the Executive Board of the Santa Clarita Economic Development Corporation and was a Foundation Board Member of Henry Mayo Newhall Memorial Hospital of Valencia, California.

About California United Bank

California United Bank, which recently celebrated the seventh anniversary of its opening, provides a full range of financial services, including credit and deposit products, cash management, and internet banking for businesses, non-profits, entrepreneurs, professionals and high net worth individuals throughout Southern California from eight full service offices in the San Fernando Valley, the Santa Clarita Valley, the Conejo Valley, Simi Valley, Los Angeles, South Bay, Anaheim and Irvine-Newport Beach. To view California United Bank’s most recent financial information, please visit the Investor Relations section of the Bank’s Web site. Information on products and services may be obtained by calling (818) 257-7700 or visiting the Bank’s Web site at www.cunb.com.

Earnings – Monday, Aug. 6, 2012

California United Bank today reported net income of $525 thousand, or $0.08 per fully diluted share, for the quarter ended June 30, 2012, which compares to net income of $312 thousand, or $0.05 per fully diluted share for the quarter ended June 30, 2011.

Second Quarter 2012 Highlights

— Net income increased by 68 percent to $525 thousand compared to $312 thousand in the second quarter of 2011; diluted earnings per share were $0.08 compared to $0.05 in the second quarter of 2011

— Pre-tax earnings increased by 85 percent to $1.03 million compared to $554 thousand in the second quarter of 2011

— Pre-tax earnings before merger expenses increased by 111 percent to $1.22 million compared to $578 thousand in the second quarter of 2011

— Total assets increased $41 million or 4.7 percent from March 31, 2012

— Total loans increased $35 million or 7.7 percent from March 31, 2012

— Total deposits grew $34 million or 4.4 percent from March 31, 2012

— Non-interest bearing deposits increased to 56.3 percent of total deposits from 55.7 percent of total deposits at March 31, 2012; cost of deposits was 0.11% for the second quarter of 2012

— Non-accrual loans declined to 1.18 percent of total loans from 1.32 percent at March 31, 2012

— Continued status as well-capitalized, the highest regulatory category. At June 30, 2012, the ratio of total capital to risk-based assets was 13.20 percent; the ratio of Tier 1 capital to risk-based assets was 11.98 percent and the Tier 1 leverage ratio was 8.57 percent.

“We are pleased to report another quarter of earnings and balance sheet growth, highlighted by record levels of pre-tax income, total assets and total deposits in the second quarter,” said David Rainer, President and Chief Executive Officer of California United Bank. “Our balance sheet growth this quarter was primarily driven by an increase in our commercial and industrial loan portfolio. We also saw an improvement in our deposit mix driven by an increase in non-interest bearing deposits from our commercial customers. We have a solid pipeline of business development opportunities, which should enable us to continue growing our CUB customer base in the second half of the year.

“Our merger with Premier Commercial Bank provides another catalyst for enhancing the value of our franchise, and we are well underway with our integration plans. Given the synergies available from this merger, we believe we can drive a material increase in the earnings power of the Bank in the future, after expenses of the merger transaction,” said Rainer.

Second Quarter 2012 Summary Results

Net Income

Net income was $525 thousand for the second quarter of 2012, an increase of $19 thousand or 3.8 percent compared to $506 thousand for the first quarter of 2012. Income for the second quarter of 2012 had $190 thousand of merger-related expenses, compared to $148 thousand of merger-related expense for the first quarter of 2012. The majority of merger-related costs are not tax deductible.

Pre-tax earnings for the second quarter of 2012 were $1.03 million, a $473 thousand or 85.4 percent increase over the $554 thousand in pre-tax earnings for same quarter of the prior year. Second quarter 2012 pre-tax earnings increased over first quarter 2012 by $71 thousand or 7.4 percent.

Return on average assets for the second quarters of 2012 and 2011 was 0.24 percent and 0.16 percent, on an annualized basis, respectively.

Net Interest Income and Net Interest Margin

Net interest income before the provision for loan losses totaled $6.9 million for the second quarter of 2012, an increase of $42 thousand or 0.6 percent over the second quarter of 2011. Although average assets increased by approximately $95 million or 12.3 percent over the past twelve months, the positive impact on net interest income was largely offset by a decline in net interest margin.

Net interest income before the provision for loan losses declined $314 thousand or 4.3 percent from the first quarter of 2012. The decline from the prior quarter is primarily attributable to a decline in net interest margin.

The Bank’s net interest income was positively impacted in both the first and second quarters of 2012 by the recognition of the discount earned on early payoffs of loans acquired from California Oaks State Bank (“COSB”) in the 2010 merger, related to the accounting requirements for acquired loans which were accounted for at fair value at December 31, 2010. The Bank recorded $237 thousand and $214 thousand in discount earned on early COSB loan payoffs in the first and second quarters of 2012, respectively.

Net interest margin in the second quarter of 2012 was 3.37 percent, compared to 3.79 percent in the second quarter of 2011 and 3.62 percent in the first quarter of 2012. The decline in net interest margin from the first quarter of 2012 is primarily attributable to a decrease in the average yield on loans to 5.56 percent from 5.71 percent, as new loans are being booked at lower rates than the existing portfolio. The Bank’s cost of funds was 0.12 percent in the second quarter of 2012 compared to 0.13 percent for the first quarter of 2012.

The Bank’s net interest margin in the second quarter of 2012 was also negatively impacted by excess liquidity held in low-yielding assets in preparation for potential balance sheet restructuring initiatives following the closing of the merger with Premier Commercial Bancorp.

Non-interest Income

Non-interest income was $752 thousand in the second quarter of 2012, an increase of $173 thousand or 29.9 percent from $579 thousand in the same quarter of the prior year. The increase was primarily due to two factors: 1) a $97 thousand increase in deposit account service charge income resulting from growth in the number and balances of the Bank’s deposit accounts; and 2) a $105 thousand increase in other non-interest income, largely resulting from non-recurring loan-related fees.

Non-interest income in the second quarter of 2012 was $130 thousand or 20.9 percent more than the first quarter of 2012. The increase was primarily due to non-recurring loan-related fees.

Non-interest Expense

Non-interest expense for the second quarter of 2012 was $6.3 million, a decrease of $171 thousand or 2.7 percent from $6.4 million for the same period of the prior year. The decrease was primarily attributable to a $162 thousand decline in FDIC deposit assessment, a $133 thousand decline in stock compensation expense, and a $123 thousand decline in OREO valuation write-downs and expenses. These decreases were partially offset by a $166 thousand increase in merger-related expenses and a $116 thousand increase in data processing expense.

Non-interest expense for the second quarter of 2012 decreased by $635 thousand or 9.2 percent from the first quarter of 2012. This decrease was primarily related to a $269 thousand decrease in salaries and employee benefits expense and a $258 thousand decrease in OREO valuation write-downs and expenses. The decrease in salaries and employee benefits expense was primarily attributable to a lower accrual for incentive compensation.

Assets

Total assets at June 30, 2012 were $908 million, an increase of $111 million or 14.0 percent from June 30, 2011 and an increase of $41 million or 4.7 percent from March 31, 2012, reflecting the growth in deposits during these periods.

Loans

Total loans were $488 million at June 30, 2012, an increase of $35 million or 7.7 percent from $453 million at the end of the prior quarter. This also represents an increase of $55 million or 12.7 percent from June 30, 2011. The increase in total loans from the end of the prior quarter was primarily attributable to 18 percent growth in the commercial and industrial loan portfolio during the second quarter of 2012.

Deposits

Total deposits at June 30, 2012 were $794 million, an increase of $34 million or 4.4 percent from March 31, 2012. This also represents an increase of $104 million or 15.1 percent from June 30, 2011. The growth in total deposits from the end of the prior quarter primarily reflects the inflow of deposits from new commercial customers.

Non-interest bearing deposits at June 30, 2012 were $447 million, an increase of $23 million or 5.5 percent from March 31, 2012. Non-interest-bearing deposits represented 56 percent of total deposits at June 30, 2012, unchanged from the end of the prior quarter.

Asset Quality

Total non-performing assets declined to $8.9 million, or 0.98 percent of total assets, from $9.1 million, or 1.05 percent of total assets, at March 31, 2012.

Of the total non-performing assets at June 30, 2012, the other real estate owned category consisted of one commercially zoned vacant lot located in Los Angeles County which is being carried on the books at $3.1 million, the estimated fair value less costs of disposition. The Bank has entered into a long-term escrow for the sale of this property, which is expected to generate net sale proceeds that approximate the net carrying value of the property. The escrow period is expected to be approximately one year.

Total nonaccrual loans were $5.8 million, or 1.18 percent of total loans, at June 30, 2012, down from $6.0 million, or 1.32 percent of total loans, at March 31, 2012.

During the second quarter of 2012, the Bank recorded net charge-offs of $546 thousand, compared with net recoveries of $17 thousand during the first quarter of 2012. Approximately $443 thousand of the net charge-offs in the second quarter of 2012 were related to one acquired loan in the COSB legacy portfolio.

The Bank recorded a loan loss provision of $380 thousand for the second quarter of 2012. The provision was primarily attributable to the growth in the loan portfolio during the quarter.

The allowance for loan losses as a percentage of loans (excluding loans acquired from the COSB acquisition, which were accounted for at fair value at December 31, 2010) was 1.67 percent at June 30, 2012, compared with 1.77 percent at March 31, 2012. The decrease in the allowance for loan losses as a percentage of loans reflects improvement in the Bank’s loan quality.

Capital

California United Bank remained well capitalized at June 30, 2012 with Total Risk Based Capital and Tier 1 Risk Based Capital ratios of 13.20 percent and 11.98 percent, respectively. All of the Bank’s capital ratios are above minimum regulatory standards for “well capitalized” institutions.

Like this:

Like Loading...

Related

Tweet This

Tweet This Facebook

Facebook Digg This

Digg This Bookmark

Bookmark Stumble

Stumble RSS

RSS

REAL NAMES ONLY: All posters must use their real individual or business name. This applies equally to Twitter account holders who use a nickname.

0 Comments

You can be the first one to leave a comment.